TL;DR: Telcos in Kenya have started masking key data points from transaction messages in compliance with the Data Protection Act. Mobile money reconciliation will, therefore, become harder for accounting teams since they rely on those data points (customer names and phone numbers) for payment attribution. As a result, cash management will be a searing headache for CFOs of fast-growing businesses leading to poor customer service, patchy debtor insights, hours lost identifying payers, etc.

Following on from our first blog post, we will be demonstrating how Churpy’s virtual accounts not only automate transaction-level and customer-level payment attribution but also alleviate the cash management pains that the Data Protection Act will cause. In the end, we provide a cool kicker, showing how virtual accounts could potentially reduce collections and reconciliation costs by 50% compared to conventional mobile money charges.

In the 3rd blog — we’ll be discussing how to reconcile bank payments (SWIFT, Pesalink, RTGS) layered on the virtual accounts technology that we have built together with NCBA Bank.

Background & Context

Over the last decade, mobile money payments have taken over as a dominant channel for P2P, C2B and increasingly, B2B payments. For example, between July 2020 and June 2021, mobile money transactions in Kenya totaled $56.7 billion in value, about 57% of Kenya’s GDP. Channels like MPesa have a far superior customer experience compared to bank-led rails due to their ease of use as well as flexible pricing for businesses.

The reality in accounts departments for allocating mobile money payments is however not as rosy. Due to the high volume of transactions, the pain of attributing payers increases with the number of transactions. Businesses have managed to take care of this using a few identifier data points, namely, the customer’s phone number and/or their name, which are sent in the confirmation messages that businesses get. However, the Data Protection Act prohibits exposing personally identifiable information (PII) which includes phone numbers and customer names in transaction messages — a move that shall make MPesa reconciliation, painstaking at scale.

“Only the first name will be passed along and the phone number of the subscriber making the transaction will be masked (obfuscated). For example, if a person named John Doe with a phone number +254721000000 makes a payment the only data that will be passed along is [John, +2547XXXXX000]”, — Business Daily

Figure1: Safaricom to hide identity of subscribers

The problem statement

For the CFOs of some of Kenya’s largest consumer-facing businesses (FMCG, property management, insurance companies, SACCOs, transport companies, utilities) and startups (e-commerce, fintech etc) whose business models are levered on mobile money (e.g. MPESA), the risk of this Act slowing down financial operations and ultimately making it impossible to run is high. Reconciliation will be very slow and reduced to a single point of failure (the transaction reference number), which in recent times has been a fraud concern. This will in turn lead to labored cash management, increase in costs and poorer controls around financial operations. There is a need to have a lasting solution that ultimately makes reconciliation easier and less error-prone.

Churpy’s solution: Virtual accounts for transaction level reconciliation and auto-receipting

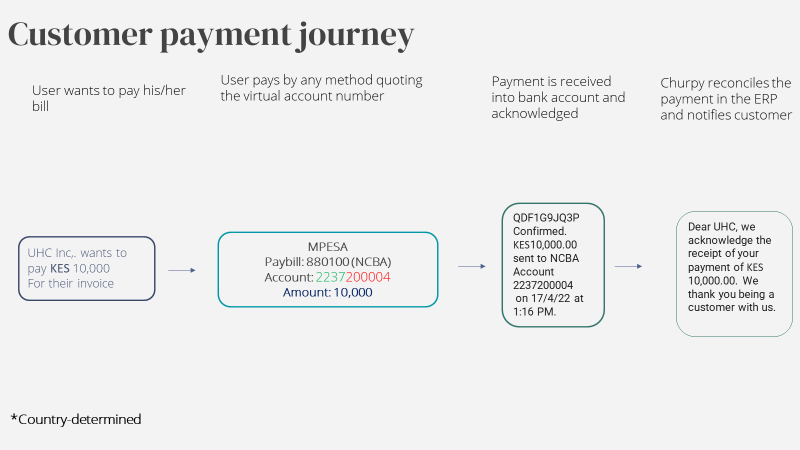

Customer flow with Churpy’s virtual accounts

When a customer wants to pay, they will be instantly issued with a virtual account, thanks to Churpy’s API that connects to your ERP and NCBA as well. For STK pushes — the virtual account number will be linked to that specific debtor transaction while for customer-initiated payments — the customer will use paybill number 880100 and quote the virtual account number in the account field. Once the payment is made, the virtual account is immediately deactivated.

Figure 2: Customer payment journey by MPESA

For the office accountant, the customer’s MPESA transaction will be automatically allocated against the open invoice or cash order, directly into the ERP, thanks to Churpy’s capability in connecting so far to 23 different types of ERPs e.g. Sage, SAP, QB and the fact that the virtual account number is directly linked to the order number.

Figure 3: Auto-allocation and auto-receipting process for 3 debtor payments

Our value proposition

- The office accountant no longer needs to use the debtor’s phone number for reconciliation. All they need to do is use the virtual account number that is unique to each customer as the key identifier. Therefore, when Safaricom obfuscates the payer information, it is still possible to identify the payer, 100% of the time.

- As a business, you will be answering the rallying call in ensuring that customer information is protected in accordance with the data protection act.

- Eliminate the need to dedicate personnel to manual reconciliation as you scale your business leading to potentially significant cost savings.

- Faster reconciliation means faster cash application/auto-receipting and better working capital availability.

- Faster reconciliation ultimately leads to a better client experience.

How we help rationalize cost of collection and reconciliation

The final piece is the cost component. With MPesa, the cost to transact for businesses and customers can be rather high. The transaction fees can be easily north of 3% depending on your tariff, in addition to harrowing reconciliation problems. The kicker with Churpy’s virtual accounts, and using the bank paybill, is that the cost is only 0.5% and, at no additional cost, we also include Churpy’s end-to-end reconciliation service to our customers. Churpy effectively becomes a channel that combines payments and reconciliation with a much lower cost quotient for the business.

For more information or to sign up on our virtual accounts service, you can email us at info@churpy.co or hit us up on Twitter @ChurpyInc.